Every enterprise has a heartbeat, and it is cash flow. Strategy, culture, and innovation matter, but none of them substitute for the ability to stay solvent while learning. Endurance is the underrated virtue of organizational life: the capacity to reinvest, to absorb shocks, to keep moving when conditions shift. Sustainability isn’t a slogan — it’s a rhythm of disciplined renewal, where insight becomes action and action becomes resilience.

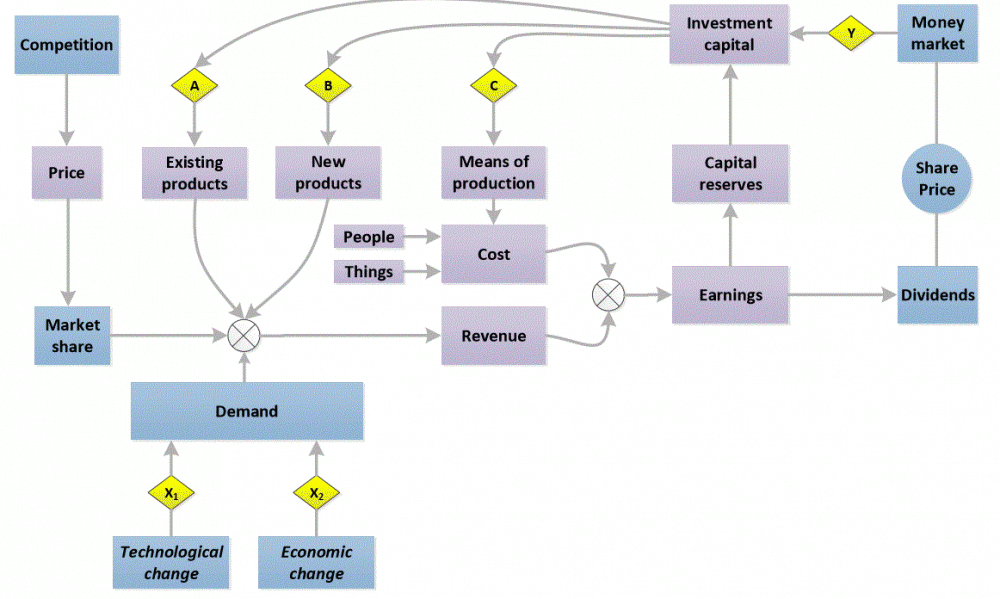

There are always limits to how much cash a business will be able to gain access to, whether through sales, borrowing, or tactical adjustments to working capital. Available cash is thus the lifeblood of businesses and serves as an important measure of the health for any business’s portfolio. This cash is generated from the many alternative sources (over different time horizons), as depicted in Figure 1.

Each business needs these reserves to invest in new product development and buffer the affordable capacity of the business against the cyclic demands placed on its resources. Once a particular product has matured in the marketplace, it becomes possible to re-purpose those resources away from mature product lines towards future ones, though achieving this goal is a long-term play.

Until this value realization is actually achieved, costs inevitably accumulate, and overruns push break-even points further and further into the future, extending the continual risk of plan continuation bias further. When seen from this lens, each product development (ad)venture exerts a tax (or drag) on a business’s resources with an expectation that these investments will result in worthwhile payoffs over a longer time horizon. Uncertainty must be factored into resource forecasts over this timeframe so that the range of likely performance is appropriately characterized. If uncertainty hasn’t been properly accounted for, or discipline wanes, gaps in performance will take longer to be noticed, since aggregation can dilute the signals available to those paying attention. Industrial models of productivity can provide a stopgap basis until more effective estimation processes are developed.

By the time reliable performance data is available and understood, it may be very difficult to avoid deterioration that can accelerate nonlinearly. For example, when we examine the robust estimate produced for a moderately complex development project for an embedded system (see attached below), the relative effects that different factors have on performance can be studied. Such estimates helpfully demonstrate how confidence levels can be accounted for when relevant productivity data forms the basis for estimates. But in the real world, useful data - appropriately cleaned and massaged into consistent structures, and at sufficient scale and type to characterize variation - is rarely available in commercial settings and has questionable relevance of the work in question has little precedent.

It is easy to understand the inherent difficulty here. Resource expenditures are typically managed separately as direct and indirect costs. Negotiations are often necessary to pro-rate these indirect costs to organizations and infrastructure across the business’s direct base. Each planning cycle must accommodate ‘carryovers’ of expenditures made in a prior accounting period but not paid until the current period is underway. As a result, each accounting method must also ‘settle accounts’ periodically. Without such reconciliation, accounting systems struggle to provide meaningful accumulations of ‘total project cost’ that are immune to gaming by those who wish to obfuscate outside interference.

A common accounting mechanism allows certain kinds of major investments that exceed an established threshold to be treated as capital expenditures. These are distinguished from annualized expenses by their multi-year distribution. Additional resources in addition to this capital investment are often necessary to acquire or prepare an asset for use, to repair or improve it for a new application, or to extend its service life. If the asset retains most of its value over an extended period after the year of acquisition, the costs may be depreciated over time and retained on the businesses’ balance sheet. If an asset has no material value shortly after its initial acquisition, it is instead treated as an item that is expensed in the accounting period in which the work was performed.

The local, regional, and national conventions underlying these rules complicate the building of reliable industry benchmarks that are relevant to most situations.

Literature on complex adaptive systems has suggested that bottom-up approaches to pursuing balance between fairness and efficiency create structures that are more resilient to volatility. Other studies have found that bottom-up activity-based costing approaches are more agile and less limiting than the top-down theory of constraints approach. Clearly, a balance must be struck.

Tradeoffs between alternatives should be performed consistently across projects and endeavors, by converting benefits to dollars using consistent and credible assumptions, meaningful measures of effectiveness, and active risk management. In practice, accounting systems may not provide data in the form needed for a meaningful analysis of alternatives. In this context, productivity measures are essential tools to stamp reality onto this ideal canvas, and to evaluate organizational performance as a whole. The underlying units of measure should be tied to the ‘real’ completion of each job, rather than just a checkmark on a schedule (which often obscures a large iceberg of remaining work).

Until a business can make credible projections of its lifecycle costs and what benefits can be expected from its products and services over realistic forecasts of the future, the yield recoverable from investments may be quite uncertain. Without a credible story of how such investments will pay off, this environment may make it increasingly challenging to secure the investments required for sustaining endeavors of significance over time. For this reason, cash surpluses should be channeled into productive uses of capital for long-term business perpetuation, such as investments to improve efficiency, accelerate the capture of new sources of revenue, and improve focus on the bottom line. While sunk costs can never be recovered, neither is it wise to bet that the cards will turn in your favor, presuming you have actually been counting them along the way.

If resilience is a rhythm, what beat is your organization marching to, and who is setting the tempo?