Economic clarity begins with naming the trade‑offs we’d prefer to ignore. The numbers are rarely the problem; the framing is. When we shift from abstract fairness to concrete consequences, decisions become less about ideology and more about survival. Accounting, in this sense, is not bookkeeping; it is a discipline of seeing the world as it is.

Investment lenses

In Knowledge and Decisions, Sowell discusses additional challenges when accounting for operating expenses using unit costs and marginal costs (which are quite different):

When people casually speak of “the” cost of producing something, they usually mean the average cost - that is, the total cost of running the enterprise divided by the number of units of output it produces. But for actual decision-making purposes at any given time, the incremental cost is more crucial. The total cost of running an airline obviously includes the cost of airplanes, but in deciding whether or not to make a particular flight, what matters at that point is whether the incremental cost of that flight will be covered by its incremental value to the passengers, as revealed by what they are willing to pay for it....

An airplane idle on the ground during a particular time has a very low cost in the economic sense of cost as a foregone alternative. If a plane that would otherwise remain in a hangar overnight is instead brought out at midnight to fly a party of vacationers to a nearby resort, the cost of this short flight that does not interfere with its other schedule of flights is much less than the “average” cost of an airplane flight. In this case, the incremental cost of the flight is little more than the cost of fuel and a flight crew, since the plane itself is there for another purpose anyway.

Thomas Sowell’s distinction between incremental and average cost exposes how easily organizations misprice risk, misread fairness, and misallocate capital.

The allocation of costs across these distinctions walks a fine line trading off among concepts that legal theory describes as fairness and efficiency. Let’s define efficiency as that which maximizes aggregate welfare, and fairness as a morally defensible treatment of or distribution among stakeholders. Different stakeholders typically benefit at different times, and to different degrees, from applying these two concepts. Achieving both goals can be quite difficult and usually requires compromises to be formed; these require trust to be developed.

Investment decisions naturally focus on the cost and payout structures of an endeavor, as embodied in the production functions of its products, services, and capabilities:

the capability to monetize outputs within a competitive and evolving landscape

the capability to project the impacts from incremental offerings under multiple scenarios

the capability to account for the inherent uncertainty characteristic for distinctive lifecycle phases

the capability to manage resources across products and phases, as new capabilities are designed, introduced, grow in usage, and reach a mature level of adoption within targeted business segments.

New product development is the seed corn for future products. Ideally, this process would be predictable and painless; the quality of construction would always exceed customer expectations; wasteful activities would occur so infrequently and have such little impact that the drain they present could be ignored.

Unfortunately, in the real world, development inevitably takes longer than forecast; risks become active issues which quickly drain available resources; and quality compromises result in traveled work, cost overruns, and dissatisfied customers. As a result, each endeavor must win a series of bets. Each product in its embryonic beginnings can be characterized as a hypothesis that investments will deliver sufficient value to the business by providing a self-sustaining source of revenue for the future. All such bets are made with lofty expectations but uncertain payoffs.

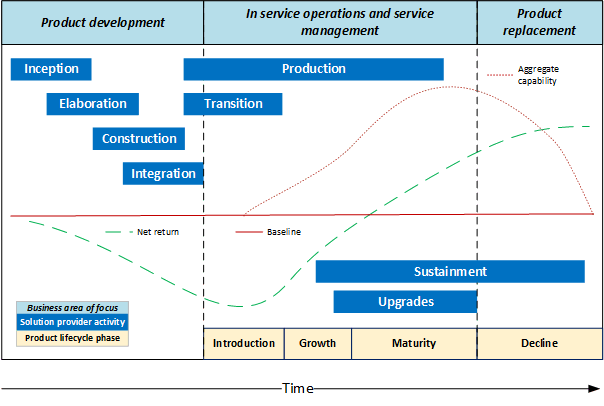

Figure 1 provides a conceptual depiction of the financial aspects of an offering over phases of its design and service life. This representation suggests consideration of alternative investments within a similar reference frame to aid in determining whether adjustments to the business’s strategies should be implemented. Unfortunately, those with self-interest in investment decisions inevitably are subject to biases and thus will manipulate factors in directions they believe to be favorable from their points of view. A counterpoint to these biases is needed.

Until a new product enters service (and investment returns begin to accrue) the resources consumed by an endeavor may well have provided better returns had they instead been allocated to alternative endeavors or investments.

The cumulative cost of these activities is depicted by the green dashed line in figure 1. A dotted red line is used to represent the aggregate capability available to users, as the product is launched, gains acceptance, achieves maturity, and declines in usage over the product’s lifecycle. A baseline business plan for a representative environment before and after realization must be available to provide a reference point that reflects the situation had no costs been incurred, and no benefits were realized. This kind of representation is also useful to highlight the continuing future obligations that may be implied by near-term commitments.

Capability development phases

An example of these groupings is depicted as blue boxes in Figure 1 above:

Inception - Customer development is performed and launch customers are selected. The business context, intentions, and ways and means by which these needs can be satisfied are defined. An endeavor to address these needs is scoped, alternative approaches are explored, and an opportunity evaluation and initial approach are defined. The cost drivers of variability in anticipated activities are considered.

Elaboration - The details required for realization are explored and evaluated. The available options are refined into definitions of a vision, requirements, and high-level architecture, within a planning baseline of the product breakdown structure. Each option is evaluated for technical and business feasibility. A down-selected set is then further elaborated into work packages, statements of work, and defined specifications so the resulting architectural elements can be concurrently realized. In parallel, mitigation options are outlined that will credibly bound uncertainty to acceptable levels. The cost drivers for this realization include the complexity and stability of the existing environment and the fitness of the business and technical architecture for these situations.

Construction - Work packages are initiated and results are verified for functional, logical, and physical design elements within the capability’s structure. The cost of developing each work package is a function of the amount of new, changed, and deprecated features which must be incorporated into the increment.

Integration- Logical and physical design elements are woven together and refined into cohesive solutions. The cost of this activity is typically driven by the quality of these design elements and the clarity of their requirements and design definitions.

Production- Physical elements of realization are sufficiently stable for replication in larger quantities. Costs are often driven by whether an effective means of late-stage customization for distinct operational configurations is in place. Note that in the PIANOS model, the above can all be considered production, when connected with the associated fields of that model.

Transition- Operational configurations are fully deployed, delivered, and readied for use within each customer environment. A service level plan is established for ongoing support. The cost driver for this activity is established by the effectiveness of upstream processes.

Sustainment- Services are provided as described in the service level plan, including support, training, troubleshooting, maintenance, and enhancements;

Upgrades- Periodic technology updates and modernization activities are performed to assure continued utility and acceptable operational performance within the bounds originally authorized.

Investors in for-profit businesses expect profits back from their investments that exceed the minimum acceptable rate of return. According to Mike Cowell, getting to cash flow neutral ((when the green line crosses the red one in figure 1) is thus an essential survival instinct for a business to develop:

What causes most businesses to fail is running out of cash. In putting together a financial plan for your startup, the primary goal is to determine when or even if the business will get to cash flow neutral. This is the point when there is the same amount of cash coming into the business as is going out...

Cash flow is the lifeblood of your business. The cash flow statement allows you to see what your cash balance will look like month to month through the duration of your plan. When looking at this statement, keep in mind you need to keep a substantial amount of cash on hand at all times as a safety buffer. It is not unusual to keep at least six months of operating expenses on hand in the form of cash. Most businesses fail because they run out of cash before they achieve positive cash flow.

Most accounting methods focus primarily on costs, rather than providing mechanisms to assure that claimed benefits are actually realistic and can be achieved under nominal circumstances. The problem with cost-focused methods is they have a built-in bias towards cutting costs and reducing expenses, rather than providing more selective shaping of investments, in concert with more effective accountability.

Enhanced collective returns are often available by reallocating existing resources from currently assigned work to pursue longer-term, more credible opportunities. A newly engineered system must enter service before its non-recurring costs can be properly accounted for as unit costs across the product’s lifecycle. The costs incurred for supporting different configurations will still need to be fairly assigned to the particular party who required those features. Profit centers and cost centers are both alternative accounting methods to achieve such a strategy, though incorporating such changes usually requires a considerable period of adjustment before the revised allocations can be fairly and efficiently distributed, and the quality of the data will be adequate for decision-making across candidate future scenarios.

Where are you using averages to comfort yourself, when increments would reveal more important truths? What additional financial information do you need to manage your situation?

Once we confront the real economics of cost, risk, and trade‑offs, the final challenge emerges: how do we sustain an endeavor over time? That requires more than accounting; it requires resilience.